Struggling With Your Mortgage in Los Angeles? You Have More Options Than You Think

A Compassionate Guide to Alternatives to Foreclosure for Greater Los Angeles Homeowners in 2026

Summary: Homeowners in Los Angeles, Beverly Hills, Pasadena, Calabasas, Woodland Hills, Tarzana, and the greater LA area facing mortgage hardship have several alternatives to foreclosure, including short sales, assumable mortgages, loan modifications, and deeds in lieu of foreclosure. Each option protects your credit differently and offers varying levels of control. This guide explains every option available to you in 2026, written by a Certified Short Sale specialist with firsthand experience helping families across Southern California.

If you're reading this, you're probably not here out of curiosity.

Something has shifted in your life. Maybe a job change, medical bills that keep growing, or the reality that your mortgage payment no longer fits the budget it once did. Whether you own a home in Glendale, a condo in Downtown Los Angeles, or a property in the San Fernando Valley, the pressure feels the same.

Whatever brought you here, first, take a breath. You are not alone, and foreclosure is not your only path.

In February 2026, there were 38,840 properties with foreclosure filings nationwide, up 20% from a year ago and marking the twelfth consecutive month of increases. Surging insurance costs, elevated interest rates, and rising HOA fees are putting real pressure on homeowners across Southern California and the entire country.

The good news? When you act early, you can often protect your credit, maintain your dignity, and move forward with far more control than you might expect.

I've guided dozens of families across Los Angeles County through these exact crossroads. As a Certified Short Sale specialist, I've made it my professional mission to understand every tool available to homeowners facing hardship, so I can offer real solutions, not just sympathy. My goal is to give you clear, honest information so you can make the best decision for your future.

Why This Is Personal to Me

I want to share something with you, because I think it matters.

Early in my career, I watched a family lose their home to foreclosure. Not because there weren't options, but because nobody told them those options existed until it was too late. They were good people. Hardworking. They had raised their kids in that house. And by the time they found me, the auction date was already set.

That experience changed the trajectory of my career. I made a promise to myself: no family I work with will ever lose their home without knowing every single option on the table first. That's why I became a Certified Short Sale specialist. That's why I study assumable mortgage strategy. And that's why I'm writing this for you today.

This isn't just a blog post. It's the guide I wish that family had found six months earlier.

What Are the Alternatives to Foreclosure?

There are four primary alternatives to foreclosure available to Los Angeles homeowners in 2026:

- Short Sale — Sell for less than owed with lender approval

- Assumable Mortgage — Transfer your low rate loan to a buyer

- Loan Modification or Forbearance — Restructure or pause payments

- Deed in Lieu of Foreclosure — Voluntarily transfer the property

Each option has different impacts on your credit, timeline, and future home buying ability. Below is a detailed breakdown.

Option 1: The Short Sale. Regain Control on Your Terms

What is a short sale? A short sale is when a homeowner sells their property for less than the outstanding mortgage balance, with the lender's approval. Homeowners pursue this option when they owe more than the home is worth and can no longer make payments.

A short sale isn't ideal, but it is often the smartest exit when continuing payments is no longer realistic. Lenders frequently agree because a short sale typically costs them far less than the full foreclosure process. As a Certified Short Sale specialist, I've navigated every complexity this process involves, from lender negotiations to buyer coordination, and I know how to move these transactions forward efficiently.

Why Los Angeles homeowners choose this route:

Less damage to your credit. Short sales typically lower your score by 50 to 150 points, compared to the 200+ point drop (and longer recovery) that often comes with foreclosure.

You stay in the driver's seat. You choose the listing price, show the home on your schedule, and participate in the process instead of having it forced upon you.

Faster path to buying again. Many homeowners become eligible to purchase another home much sooner after a short sale than after a foreclosure. This matters deeply in competitive markets like West Los Angeles, Santa Monica, and Burbank, where timing your re-entry can mean the difference between finding a home and being priced out.

Dignity and closure. This route allows you to exit on your timeline instead of facing the public stress of an auction or eviction.

Time matters. The earlier you explore a short sale, the more options and leverage you have.

How a Short Sale Saved a Woodland Hills Family

Last year, I received a call from a couple in Woodland Hills who had fallen behind on their mortgage after a medical emergency. They had two kids in the local schools, a home they loved, and a growing sense of panic. They assumed foreclosure was inevitable.

It wasn't.

After reviewing their situation, I determined that a short sale was their strongest option. Their home was underwater due to a combination of the rate environment and deferred maintenance. I negotiated directly with their lender, managed the listing strategy to attract qualified buyers quickly, and within four months, the sale closed. Their credit impact was minimal. The deficiency was forgiven. And most importantly, they walked away with the ability to rebuild, on their terms.

Today, that family is renting comfortably in the same Woodland Hills school district, rebuilding their credit, and on track to buy again within two years. That's what the right strategy can do.

Related: See our guide to buying and selling in Woodland Hills and Calabasas →

Option 2: The Assumable Mortgage. Your Hidden Luxury Asset

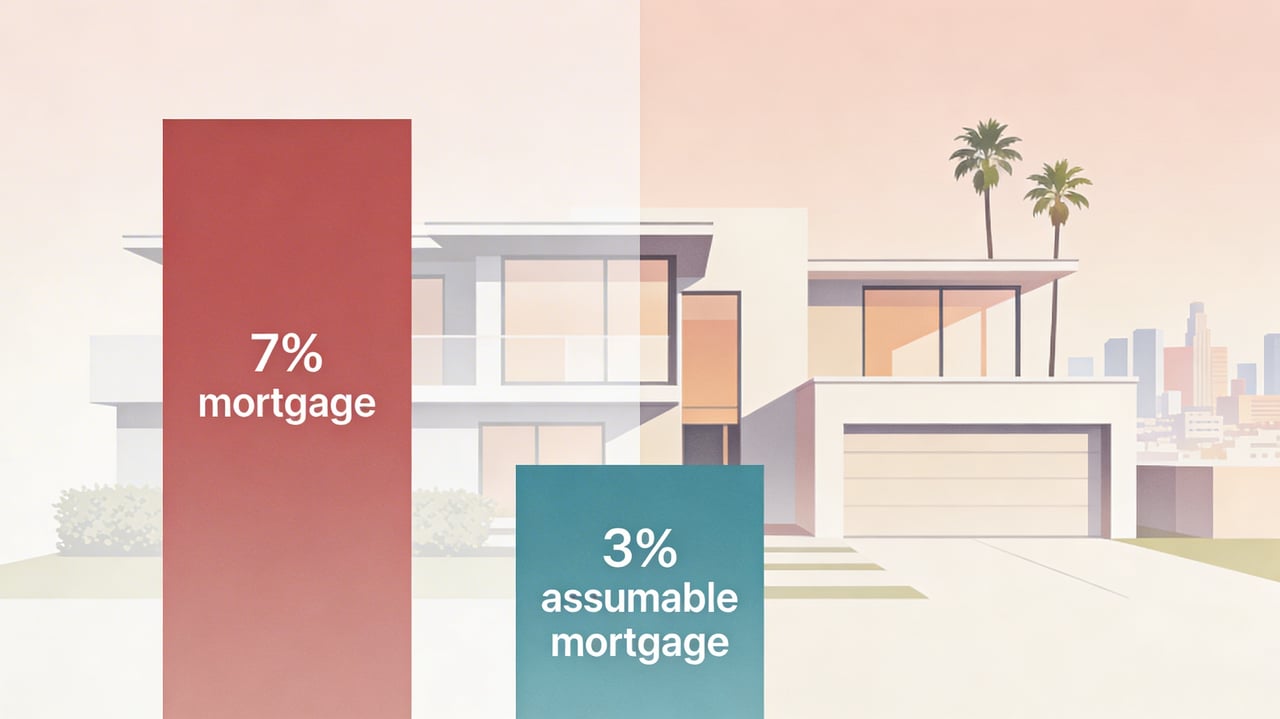

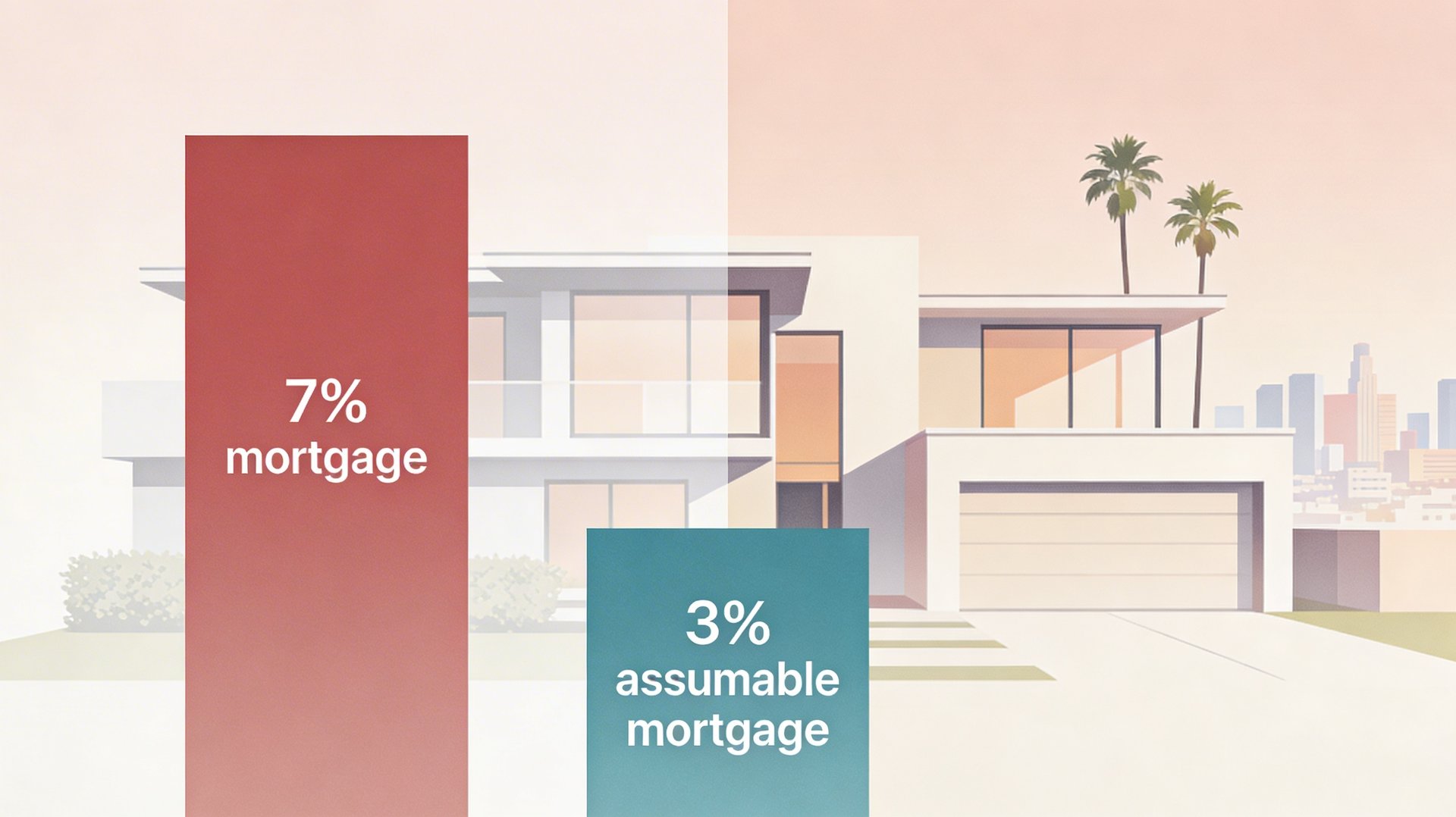

What is an assumable mortgage? An assumable mortgage is a type of home loan that allows a buyer to take over the seller's existing mortgage, including the interest rate, remaining balance, and repayment terms. FHA, VA, and USDA loans are typically assumable with lender approval.

Here's something most homeowners still don't realize: your mortgage may be one of the most valuable features of your home right now.

If you have an FHA, VA, or USDA loan originated between roughly 2020 and 2022 with a rate between 2% and 4%, it is likely assumable. This means a qualified buyer can take over your existing low interest loan instead of getting a new one at today's higher rates.

Why this matters for Los Angeles sellers

For buyers, the savings are life changing. On a $400,000 loan balance, moving from a 7% rate to a 3% rate can save roughly $974 per month, more than $200,000 over the life of the loan. In neighborhoods like Silver Lake, Culver City, or Encino, that savings is the difference between affording the home or not.

For you as a seller, it becomes a powerful marketing advantage that can attract more offers and help your home stand out in a competitive market.

Recent estimates show about 6 million homes across the U.S. carry both an assumable mortgage and a rate below 5%. Yet the vast majority of eligible sellers have no idea this opportunity exists.

If you hold one of these loans, your home isn't just another listing. It's a premium opportunity for the right buyer. We should talk about how to position this strategically.

How an Assumable Mortgage Turned a Calabasas Crisis Into a Premium Sale

One of my most memorable transactions involved a homeowner in Calabasas who was facing a job relocation and couldn't afford to carry two mortgages. She was days away from listing at a reduced price just to get it done quickly.

During our initial consultation, I reviewed her loan documents and discovered she had an FHA loan from 2021 at 2.75%. She had no idea it was assumable.

We repositioned the entire marketing strategy around that loan. Instead of a desperate price reduction, her home became one of the most attractive listings in the area. Buyers weren't just purchasing a beautiful Calabasas property, they were inheriting a mortgage that would save them nearly $1,000 per month compared to current rates. We received multiple offers within two weeks. She sold above her original asking price, avoided any financial distress, and relocated with confidence.

That's the power of knowing what you have before you make a decision out of fear.

Assumable Mortgage vs. Traditional Mortgage: Quick Comparison

| Feature | Assumable Mortgage | New Mortgage (2026) |

|---|---|---|

| Interest Rate | 2% to 4% (locked) | ~6% to 7% |

| Monthly Payment ($400K) | ~$1,686 (at 3%) | ~$2,661 (at 7%) |

| Lifetime Interest Savings | $200,000+ | — |

| Available Loan Types | FHA, VA, USDA | All types |

| Seller Advantage | Significant | Standard |

Related: Explore our Los Angeles neighborhood guides →

Option 3: Loan Modification or Forbearance. Stay in Your Home

What is a loan modification? A loan modification permanently changes the terms of your existing mortgage, such as the interest rate, loan term, or principal balance, to make monthly payments more affordable.

What is forbearance? Forbearance is a temporary agreement with your lender to reduce or pause mortgage payments during a period of financial hardship.

Sometimes the best move isn't selling at all. Lenders are often more flexible than their public messaging suggests. A loan modification can lower your monthly payment by adjusting the rate, extending the term, or forgiving a portion of the principal. Forbearance can temporarily pause or reduce payments while you regain stability.

This path is especially valuable when your hardship feels temporary, whether from illness, job transition, or an unexpected expense. For homeowners in areas like Woodland Hills, Tarzana, or Arcadia who love their community and schools, staying put may be the best long-term financial decision.

When Staying Put Was the Right Move for a Tarzana Homeowner

Not every story ends with a sale, and that's a good thing.

A homeowner in Tarzana reached out to me last spring, overwhelmed after his small business had a rough quarter. He was two months behind on his mortgage and assumed he'd need to sell the beautiful home he'd spent years renovating, the home where his daughter had just started at a nearby school she loved.

After sitting down with him, it was clear his hardship was temporary. His business pipeline was strong. He just needed breathing room. Instead of listing his home, I connected him with the right resources and walked him through the loan modification process step by step. His lender agreed to a temporary forbearance, followed by a modification that lowered his monthly payment by $400.

He's still in that home today. His daughter is still in that school. And he calls me every few months just to say thanks.

Sometimes the best real estate advice is: don't sell. Not yet.

It's about creating a sustainable future in the home you love.

Option 4: Deed in Lieu of Foreclosure. A Graceful Exit

What is a deed in lieu of foreclosure? A deed in lieu of foreclosure is a voluntary agreement where the homeowner transfers ownership of the property to the lender in exchange for being released from the remaining mortgage debt, avoiding the formal foreclosure process.

When other options have been exhausted, a deed in lieu allows you to voluntarily transfer the property back to the lender in exchange for releasing you from the debt. You avoid the lengthy public process of foreclosure and maintain more privacy and dignity.

This can be the kindest choice for yourself when staying is no longer possible.

This option may be right for you if:

- You've exhausted other options

- You want to avoid the public stigma of foreclosure

- You need a clean break to move forward

Why These Options Matter More in Greater Los Angeles in 2026

Mortgage rates are widely expected to hover near 6% for the foreseeable future. That "lock in effect" continues to limit inventory across Los Angeles, meaning there are fewer homes available and sellers who do list have significant leverage.

This actually makes assumable low rate loans even more valuable for sellers who must transition. Whether you're in a luxury property in Bel Air, a family home in Woodland Hills, a retreat in Calabasas, or a starter in Tarzana, your low rate loan could be the most compelling selling point you have.

The worst move right now is waiting in silence. Knowledge truly is power here.

The Bottom Line: You Still Have Choices and Power

Foreclosure can feel traumatic because it removes your voice. A short sale, assumable mortgage strategy, loan modification, or deed in lieu puts you back in control.

I've seen it firsthand, with the Woodland Hills family who rebuilt after a short sale, the Calabasas homeowner who turned a crisis into a premium sale through an assumable mortgage, and the Tarzana father who stayed in his home because we found the right modification. Every situation is unique. Every homeowner deserves to know their options.

As a Certified Short Sale specialist with deep experience in assumable mortgage strategy across the greater Los Angeles area, I can tell you with confidence: there is almost always a better path than foreclosure when you act early.

Remember this:

✓ Your situation is not hopeless. ✓ Your options are real. ✓ Time is your most valuable asset right now.

Let's Talk. Privately and Without Pressure

If any part of this resonates, I would be honored to speak with you confidentially. No judgment. No hard sell. Just clear answers tailored to your circumstances, whether that means leveraging an assumable mortgage as a luxury selling feature, navigating a short sale with minimal impact, or exploring ways to stay in your home.

I serve homeowners across the Greater Los Angeles area, including Calabasas, Woodland Hills, Tarzana, Beverly Hills, Santa Monica, Pasadena, Glendale, Burbank, Encino, Sherman Oaks, the San Fernando Valley, Downtown LA, Long Beach, and all surrounding communities.

Schedule Your Confidential Consultation →

Because the path forward may look different than you imagined, but it can still lead somewhere beautiful.

Frequently Asked Questions

What is the best alternative to foreclosure in Los Angeles? A short sale is often the best alternative for Los Angeles homeowners because it causes less credit damage, allows you to maintain control of the sale process, and may allow you to buy again sooner than after a foreclosure. Working with a Certified Short Sale specialist ensures the process is handled correctly.

What is an assumable mortgage and can I use it to sell my home? An assumable mortgage allows a buyer to take over your existing loan, including its lower interest rate. If you have an FHA, VA, or USDA loan from 2020 to 2022, your loan is likely assumable, which can be a significant competitive advantage when selling your home in Calabasas, Woodland Hills, Tarzana, or anywhere in Los Angeles.

How much does a short sale hurt your credit? A short sale typically lowers your credit score by 50 to 150 points, compared to 200 to 300 points for a foreclosure. Recovery time is also generally shorter.

Can I buy a home again after a short sale? Yes. Many homeowners who complete a short sale become eligible to purchase another home sooner than those who go through foreclosure, sometimes with certain restrictions.

How do I know if my mortgage is assumable? Check your original loan documents or contact your lender directly. FHA, VA, and USDA loans are generally assumable. Conventional loans typically are not.

What areas in Los Angeles do you serve? I serve homeowners throughout Greater Los Angeles, including Calabasas, Woodland Hills, Tarzana, Beverly Hills, Bel Air, Santa Monica, West Hollywood, Pasadena, Glendale, Burbank, Encino, Sherman Oaks, Culver City, Downtown LA, Silver Lake, Long Beach, Torrance, and all surrounding communities.

Are you a Certified Short Sale specialist? Yes. I am a Certified Short Sale specialist with extensive experience navigating lender negotiations, buyer coordination, and complex distressed property transactions across the greater Los Angeles area.

Nathaniel Getzels The Getzels Group | Coldwell Banker Global Luxury, Certified Short Sale Specialist Licensed Real Estate Expert Serving Greater Los Angeles Specializing in Luxury Transitions, Assumable Mortgage Strategy, and Distressed Property Solutions (818) 535-5337 |